- 01/06/2026

- Govind S. Jethani

- 206 Views

- 2 Likes

- Tax

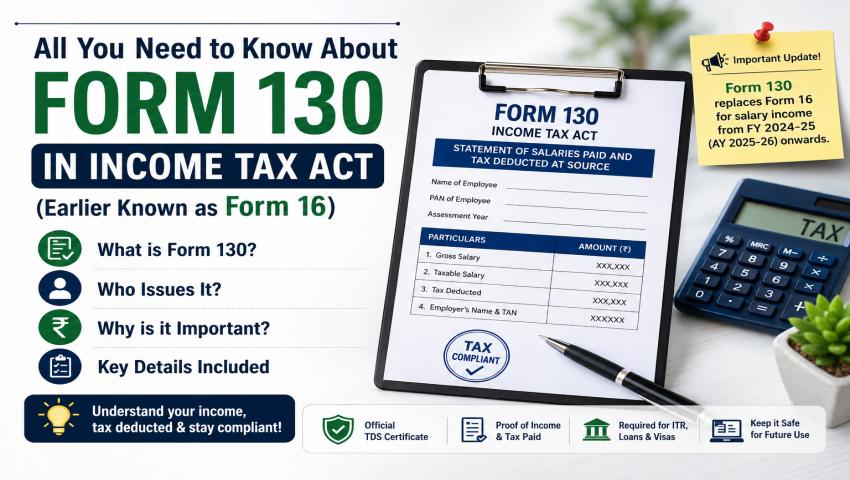

All You Need to Know About Form 130 in Income Tax Act (Earlier Known as Form 16)

For salaried employees, Form 16 has always been one of the most important income tax documents. Every year, employees wait for it before filing their Income Tax Return (ITR). It contains salary details, tax deducted by the employer, exemptions, deductions, and other important tax-related information.

Now, under the new Income-tax Act, 2025 framework, Form 16 is being referred to as Form No. 130. While the name and structure are changing, the core purpose remains almost the same. In this comprehensive guide by My Finance Gyan, we break down everything you need to know about how Form 130 in income tax will continue to function as the primary salary TDS certificate issued by employers.

As per the Income Tax Department FAQ, Form No. 130 is an annual certificate for Tax Deducted at Source (TDS) issued by an employer to a salaried employee or pensioner. It contains details of salary earned, tax deducted and deposited, and applicable deductions. It also helps employees claim TDS credit while filing their income tax return.

What is Form 130?

Form 130 in income tax is the new salary TDS certificate under the updated tax framework. Earlier, employees knew this document as Form 16.

In simple words, Form 130 shows:

- Your salary income

- The amount of tax deducted by your employer

- Whether the deducted tax has been deposited with the Government

- Deductions and exemptions considered

- Taxable salary calculated by the employer

For salaried taxpayers, Form 130 will remain one of the most important documents required while filing ITR.

It is important to understand that Form 130 is not a new tax. It is primarily a renumbered and updated form under the revised Income-tax Act and Rules.

When Will Form 130 Apply?

As per available information, Form 16 is expected to be renumbered as Form 130 from 1 April 2026 under the new Income-tax Act, 2025 and Income-tax Rules, 2026 framework. Reports and tax updates suggest that the change will apply from Tax Year 2026-27 onwards.

For earlier years, employees may still continue to use and refer to Form 16. Therefore, older payroll records, HR systems, and tax portals may continue displaying the old terminology for previous financial years.

Who Issues Form 130?

Form 130 is issued by the employer.

If your employer deducts TDS from your salary, they are responsible for issuing this certificate. The document helps employees verify whether the tax deducted from salary has actually been deposited with the Government.

For pensioners as well, Form 130 may apply wherever TDS is deducted from pension income. The Income Tax Department FAQ also mentions its application to specified senior citizens in relation to specified interest income under the new Act.

Why is Form 130 Important?

Form 130 is important because it connects your salary income with your Income Tax Return.

Many employees file their ITR primarily based on Form 130 (earlier Form 16). However, taxpayers should not blindly rely only on this document. It is always advisable to cross-check information with AIS, Form 26AS, bank interest statements, capital gains, house property income, freelance income, and other sources of income.

Still, for salary income reporting, Form 130 in income tax remains highly useful.

It helps employees verify:

- Correct PAN details

- Correct salary amount

- Proper TDS deduction

- Deductions and exemptions considered

- Whether TDS has been deposited

- Possible mismatches before filing ITR

If there is any mistake in Form 130, employees should immediately contact their employer or payroll department for correction before filing the return.

Parts of Form 130:

As per the Income Tax Department FAQ, Form No. 130 consists of three parts: Part A, Part B, and Part C.

Part A:

Part A generally contains:

- Employer details

- Employee details

- PAN and TAN

- TDS deduction details

- Tax deposit information

Part B:

Part B includes:

- Salary breakup

- Exemptions

- Deductions

- Taxable income calculation

Part C:

Part C may contain additional prescribed information as specified under the updated form structure.

Although the format may look different from the earlier Form 16, the practical purpose remains similar for salaried taxpayers.

What Details Should Employees Check in Form 130?

Employees should carefully review Form 130 instead of simply downloading and using it directly for filing.

Important details to verify:

- Name and PAN details

- Employer name and TAN

- Assessment Year and Tax Year

- Gross salary details

- Allowances and perquisites

- Deductions and exemptions

- Taxable salary calculation

- TDS deducted and deposited

Employees should also confirm whether deductions under:

- Section 80C

- Section 80D

- NPS contributions

- Home loan interest

- Other eligible deductions

have been correctly considered wherever applicable.

Additionally, taxpayers should match the TDS amount with AIS and Form 26AS/Form 168 (once applicable). Ignoring mismatches may create issues during ITR processing.

Can You File ITR Without Form 130?

Yes, technically you can file your Income Tax Return without Form 130 using:

- Salary slips

- AIS

- Form 26AS/Form 168

- Bank statements

- Other financial records

However, in practical terms, Form 130 simplifies the entire filing process because it provides consolidated salary and TDS information directly from the employer.

If your employer has deducted TDS but failed to issue Form 130, you should follow up with the HR or payroll department immediately.

Difference Between Form 16 and Form 130:

The primary difference is the form number and legal reference under the updated tax law framework.

- Form 16 existed under the Income-tax Act, 1961

- Form 130 is linked with the Income-tax Act, 2025 framework

Tax updates also indicate that salary TDS references are shifting to revised section mappings under the new Act.

For employees, the practical understanding is simple: Form 130 is replacing the familiar Form 16 terminology for salary TDS certificates.

The underlying tax calculation process does not automatically change just because the form number has changed.

What Employers Should Keep in Mind?

Employers should update:

- Payroll systems

- HR communication

- Employee tax declaration formats

- TDS certificate references

Many employees may initially get confused seeing Form 130 instead of Form 16. Therefore, employers should clearly communicate that Form 130 is simply the new name for the salary TDS certificate.

Employers must also ensure:

- Correct TDS deduction

- Timely TDS deposit

- Proper return filing

- Accurate certificate issuance

Any mismatch can create complications for employees during ITR filing and processing.

Common Mistakes Employees Should Avoid:

Employees should avoid the following common mistakes:

- Filing ITR without checking Form 130 carefully

- Ignoring mismatches between Form 130 and AIS

- Assuming all deductions are automatically allowed

- Forgetting to report other sources of income

- Using Form 16 details for the wrong tax year

- Not requesting correction of errors from the employer

It is important to remember that employers generally deduct TDS only on salary income. If you have:

- Interest income

- Capital gains

- Rental income

- Freelance income

- Business income

you must separately report those incomes in your ITR.

Final Thoughts:

Form 130 is essentially the new name and revised format for the salary TDS certificate previously known as Form 16. For salaried employees, it will continue to remain one of the most important documents for filing income tax returns.

Employees should not treat it as just another form. Always verify the details carefully, match TDS with tax records, confirm deductions, and properly disclose all other income sources while filing returns.

The name may change from Form 16 to Form 130, but the purpose remains the same — helping employees verify salary income, TDS deduction, and tax credit while filing their Income Tax Return.

Disclaimer: The views expressed in this article/blog are personal and solely for educational and awareness purposes. The content is not intended to provide professional tax, legal, or financial advice, nor does it recommend any specific product or service.