- 15/06/2026

- Govind S. Jethani

- 141 Views

- 2 Likes

- Tax

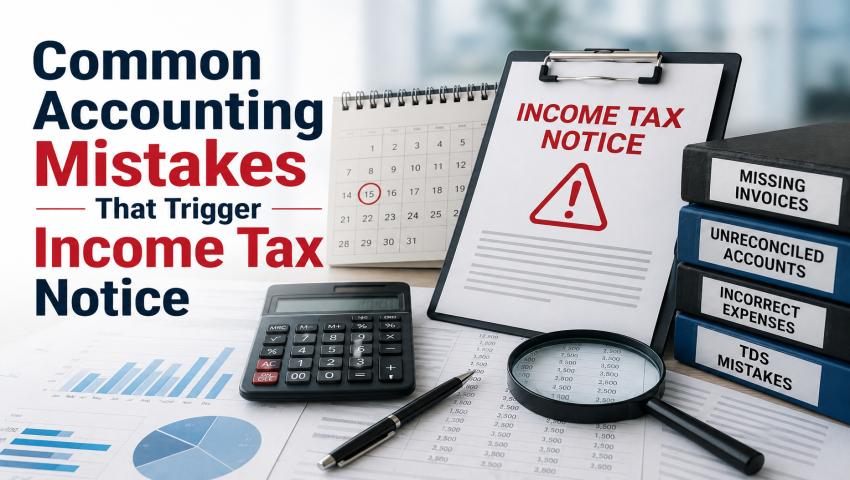

Common Accounting Mistakes That Trigger Income Tax Notice

Every small business owner, startup founder, and salaried professional in India shares a common goal: growing their hard-earned money smoothly. But while you focus on sales, operations, or your career, a tiny slip-up in your books of accounts can quickly put you on the radar of the tax authorities.

Today, managing your accounts isn’t just about keeping rough diaries or maintaining raw excel sheets. Even a minor mathematical error or a missed reporting entry can bring an official communication straight to your inbox. In this masterclass guide, My Finance Gyan is your guide for this blog to decode exactly why these slips happen, how the tax department catches them instantly using automated tracking, and how you can safeguard your business or personal finances from a sudden tax scare.

What Is an Income Tax Notice?

1. Meaning of Income Tax Notice:

An income tax notice is an official legal communication sent to you by the Income Tax Department. Think of it less as an accusation and more like a formal query. The department sends these notices when they require specific information, need you to clarify suspicious transactions, want to correct computational errors, or need to verify whether the tax paid matches your real economic activities.

2. Why the Income Tax Department Sends Notices:

The system doesn’t pick taxpayers completely at random anymore. Instead, specific anomalies flag your profile. The primary income tax notices reasons include:

- Mismatch in income reporting: What you declare in your return doesn’t tie up with what your bank or employer reports.

- Incorrect deductions: Claiming tax exemptions or relief under various chapters without holding valid, verifiable proof.

- High-value transactions: Making large purchases, investments, or cash deposits that look completely disproportionate to your declared income slabs.

- Late filing or non-filing of returns: Missing statutory deadlines while your financial footprints indicate you are fully liable to pay tax.

- Suspicious financial activity: Frequent cash handling, round-tripping, or booking unexpected losses that don’t match general business logic.

How the Income Tax Department Detects Accounting Errors?

Gone are the days of manual file-checking where errors went unnoticed. Tax administration has shifted into a fully computerized environment.

1. Use of AIS and Form 26AS:

The department tracks your entire economic life through two primary documents: the Annual Information Statement (AIS) and Form 26AS. The AIS tracks comprehensive data—interest from savings accounts, recurring deposits, stock market investments, mutual fund purchases, and foreign remittances. If your bookkeeping fails to account for even one of these items, a clear data mismatch occurs instantly.

2. Data Analytics and Automated Scrutiny:

Under the current system framework, the department relies on predictive intelligence and deep data-matching systems. High-powered servers match data cross-platform:

- GST vs. ITR Comparison: Your reported sales turnover on the GST portal is matched directly against the gross turnover listed in your Income Tax Return (ITR).

- Bank Account Monitoring: Automated algorithms run continuous flags on banking sectors, reading aggregate cash inflows across all savings and current accounts linked to your Permanent Account Number (PAN).

Common Accounting Mistakes That Trigger Income Tax Notice:

Let’s look into the specific accounting errors that frequently result in tax scrutiny:

1. Mismatch Between Income and Bank Transactions:

Many taxpayers think that if an income stream isn’t mentioned in a Form 16, it doesn’t need to be declared. If your bank account receives steady credits or sudden lump-sum inflows, but your filed ITR reflects a significantly lower income, the system flags it. Similarly, unexplained cash deposits into savings accounts during festive seasons or business cycles are common income tax notice reasons.

2. Incorrect Reporting of Business Expenses:

Proprietors and small businesses often try to lower their net profit by routing personal lifestyle expenses—like family vacations, fuel for personal cars, or personal restaurant dining—directly through business books. Without valid commercial invoices, proper vouchers, or clear business connection, these claims fail during audits and trigger severe notices.

3. Errors in GST and Income Tax Data:

If your monthly or quarterly GST returns (like GSTR-1 or GSTR-3B) state a total annual turnover of ₹75 Lakhs, but your financial balance sheet filed under ITR shows a turnover of ₹60 Lakhs, an automated red flag goes off. Any difference in sales reporting or claiming mismatched Input Tax Credit (ITC) between systems will bring an electronic inquiry to your doorstep.

4. Failure to Maintain Proper Books of Accounts:

Scattering vendor bills across email folders, losing physical cash receipts, or ignoring basic double-entry bookkeeping principles makes it impossible to file a clean return. If you can’t back your balance sheet figures with actual paperwork during a routine check, your reported numbers are labeled unverified.

5. Claiming Wrong Deductions and Exemptions:

Attempting to maximize tax savings by entering arbitrary numbers under Section 80C, 80D, or house rent allowances without paying real rent or holding premium receipts is an invitation for a defective return notice. Automated checking protocols catch these unsupported deductions easily.

6. Non-Reporting of Additional Income:

It is mandatory to disclose all secondary streams of income. This includes:

- Freelancing gigs or side consultations.

- Interest earned on savings accounts and fixed deposits.

- Rental income from residential or commercial properties.

Short-term or long-term capital gains from selling stocks, mutual funds, or cryptocurrency assets.

7. TDS Mismatch Issues:

If an enterprise or client deducts Tax Deducted at Source (TDS) on your behalf but records it under an incorrect PAN, or if you claim a higher TDS credit in your return than what is visible on your updated Form 26AS, the tax clearing system holds back your processing and issues a warning.

8. Cash Transactions Beyond Permissible Limits:

Accepting cash loans or repayments of ₹20,000 or more, or dealing in business expenses over ₹10,000 per day in physical cash, directly violates the law. High cash deposits without identifiable operational roots are a surefire way to trigger an investigation.

9. Late Filing or Revised Return Errors:

Filing returns past the statutory due date invites interest, penalties, and closer scrutiny. Furthermore, filing multiple revised returns within a few weeks to repeatedly adjust income or add sudden deductions looks highly suspicious to automated risk-assessment engines.

10. Using Multiple Bank Accounts Without Proper Disclosure:

Taxpayers are legally required to disclose every single active bank account held in their name when filing an ITR. Attempting to manage operational flows through a secondary, undisclosed account to hide transactions creates a highly damaging trail once caught by the department’s linked database.

Consequences of Accounting Mistakes:

Ignoring proper financial data entry isn’t just an administrative error—it has real commercial and legal consequences:

How to Avoid Accounting Mistakes?

- Establish Digital Bookkeeping: Move away from physical diaries. Adopt reliable accounting software to record every invoice, payment, and expense entry right when it occurs.

- Perform Periodic Reconciliations: Reconcile your internal sales ledger with your bank statements and GST filings every single month to catch data variations early.

- Verify Document Trails: Store your receipts, purchase bills, loan statements, and investment proofs digitally inside structured cloud folders for quick access.

- Run Pre-Filing Verifications: Before uploading your ITR, cross-check your finalized trial balance figures line-by-line against your live AIS, TIS, and Form 26AS portals.

- Engage Professional Counsel: Have an experienced Chartered Accountant or financial advisor audit your files before final submission to identify potential compliance gaps.

Latest Income Tax Compliance Trends in India:

Tax administration in India has fully transformed into a tech-first ecosystem. The department relies heavily on advanced data engines to screen returns. This technology monitors e-way bills, e-invoicing data, bank registries, and digital wallets continuously.

The focus has shifted sharply toward real-time transaction tracking. This means discrepancies are often flagged via automated emails and SMS notifications almost immediately after filing. For small and medium enterprises (SMEs) and early-stage startups, keeping transparent, accurate, and digitally verifiable books of accounts from day one is no longer optional—it is a core business requirement.

Conclusion:

At the end of the day, an income tax notice isn’t something to panic over, but it is a clear sign that your accounting process needs immediate attention. Most compliance issues and tax scares stem directly from basic bookkeeping oversights, delayed data reconciliation, or unverified expense claims.

By building clear accounting workflows, leveraging smart software solutions, and verifying your data against official portals like the AIS, you can keep your business smooth, stress-free, and fully compliant. Take control of your financial records today, run timely internal reviews, and always consult a qualified tax professional to ensure your financial growth remains completely protected.